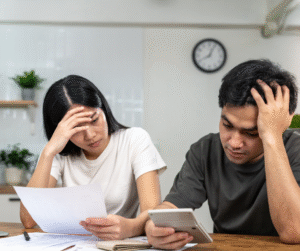

Summer vacation is supposed to be stress-free, but for Minnesota homeowners, the weeks spent away from home introduce a feeling of anxiety they can’t shake. Between unpredictable summer storms, rising humidity, and the increased chance of a break-in, an empty home is more vulnerable than most families realize. A little preparation before you leave can mean the difference between coming home refreshed and coming home to a costly mess. This checklist walks you through everything you need to do before you pack your bags, so you can enjoy every moment of your trip knowing your home is in good hands. Summer-Specific Home Risks Minnesota Homeowners Should Know Most people associate home risks with winter, which is understandable. Frozen pipes, ice dams, and the bitter cold are all real concerns, especially here in Minnesota. But summer brings its own set of challenges that we need to prepare for. Our summers are known for intense thunderstorms that can roll in fast and hit hard. This heavy rainfall can cause basement flooding, particularly in older homes or properties in low-lying areas. Without anyone at home to catch a problem early, a small amount of water in the basement can lead to significant structural damage and mold growth in a matter of days. On top of that, a power outage during a storm can knock out your sump pump just as water is rising in your basement. Heat and humidity pose their own risks, too. If your air conditioning fails while you're away, indoor temperatures and moisture levels can climb quickly. That kind of environment is a breeding ground for mold and can cause damage to wood floors, furniture, or even drywall. Then there’s the security angle. Homes that look visibly unoccupied are a common target for summer break-ins. Overflowing mailboxes, uncut lawns, and houses without lights on are clear signs to burglars that your home is empty. Your Pre-Departure Home Security Checklist Running through a simple checklist before you leave takes less than an hour and can save you from a very unwelcome homecoming. Arrange for someone to pick up your mail and packages. Set timers inside so lights turn on in common areas at night. Make sure every window and door is locked and secured, including side garage doors, basement windows, and sliding glass doors. For longer trips, set up landscaping services so your lawn stays well-kept. Protecting Against Water Damage and Storm Issues Minnesota’s summer storm season brings another very real and serious risk for unattended homes: water damage! Here are some ways that you can protect your home from costly water damage: Clear out gutters and downspouts Check that your sump pump is working properly Consider turning off your home’s main water supply to eliminate the risk of a burst pipe or slow leak causing issues Unplug non-essential appliances and electronics to prevent a power surge during a summer storm A few minutes of preparation before you leave can protect both your belongings and your home – and your peace of mind! What Your Homeowners Insurance Covers (and Doesn't) Even when you've done everything right, sometimes things still go wrong. That's exactly what homeowners insurance is there for! Going over your policy before you leave will help you feel more comfortable staying away for longer periods. Most standard homeowners policies cover sudden, unexpected events like storm damage, fire, theft, and certain types of water damage. For example, if a tree falls on your roof during a storm or someone breaks in while you're away, it will typically be covered. What generally isn’t covered is damage that results from negligence. If the problem was foreseeable and preventable but ignored, that could cause issues in your claim. For example, if your sump pump has been failing for months and you didn't address it before leaving, a resulting flood may not be fully covered. Insurance companies often look at whether the homeowner exercised "reasonable care" in maintaining and protecting their property. As you go through your prevention checklist, document exactly what you did. Take photos of your home's condition before your trip, keep receipts for any maintenance work you have done, and hold on to any records of sump pump inspections or appliance servicing. That documentation can come in handy if your claim is disputed. Smart Technology and a Communication Plan Take your preparation to the next level by pairing it with a few smart home tools for an added layer of protection. Tools like water leak sensors placed near appliances, water heaters, and sump pumps, a smart thermostat, or security cameras can help keep your home safe and sound while you’re enjoying your time away. In addition to these smart tools, always ask a trusted neighbor, friend, or family member to keep an eye on your home while you’re gone. Make sure your emergency contact has everything they need to act quickly if something comes up: a spare key, your alarm code, your insurance agent's number, and a way to reach you while you're traveling. Before You Go: Key Takeaways A summer vacation should leave you feeling refreshed, not anxious about what might be happening back home. The steps covered in this guide are smart habits that every Minnesota homeowner should build into their pre-trip routine. Here's a quick recap of the most important things to do before you leave: Make your home look lived in with light timers, collected mail, and maintained landscaping Lock all doors and windows Clear gutters, test your sump pump, and consider shutting off the main water supply Unplug non-essential electronics and appliances to guard against power surges Set up smart home sensors and give a trusted contact everything they need to act in an emergency Document your pre-departure steps in case you ever need to support an insurance claim One more thing that belongs at the top of every pre-vacation checklist: making sure your homeowners insurance coverage is actually up to the job. Policy details matter, and gaps in coverage have a way of showing up at the worst possible time. Before you head out this summer, take a few minutes to review your homeowners policy with the team at Rehm Insurance. As Mankato's locally owned, independent agency, we know Minnesota homes and the risks they bring. We'll make sure your coverage is solid so you can enjoy every day of your trip with total peace of mind. Give us a call at (507) 345-3366 or request a free quote online today.

Minnesota storm season doesn't mess around! This guide helps Minnesota families actually prepare for severe weather before the sirens go off.

If you know me at all, you know I’m not just the guy who helps protect your home and business. I’m also the guy who will talk fishing with you for hours if you let me. So when I came back from a recent trip to Yellowstone country, fresh off catching Yellowstone cutthroat trout in Montana, we figured there was no better time to write a blog about something near and dear to my heart… fishing. And more specifically, fishing right here in Southern Minnesota.